Archive for October 30th, 2011

Introduction to Management 101 no comments

I have been reading David Boddy’s ‘Management an introduction’ (4th edition). It’s a useful introduction to the different ways in which management has emerged as a social science, including the main theoretical perspectives on management.

Interestingly, the first case study is Ryanair and how its managers were quick to spot the potential of the Web by opening www.ryanair.com as a booking site in 2000. Within a year it was selling 75% of seats online, and now sells almost all seats this way.

In considering what ‘management’ is, an important component is innovation. Computers and network (the new agents of communication) has propelled management into the new economy through innovation. To give one simple example from Boddy, the use of emails has sped up communication enabling managers to strengthen their interpersonal roles.

Thus, it seems to me that technology (including the Web) is both an external and internal force upon management: it facilitates innovation to beat the external competition; while also providing an opportunity for corporate entities to streamline themselves internally via more efficient working practices. In the nature of a double-edged sword, however, it may also be the undoing of those businesses that do not use them efficiently.

As Boddy points out, everywhere the Web is enabling great changes in how people organise economic activity, equivalent to the Industrial Revolution in the 19/20th century. This includes the challenges of coping with the transition to a world in which ever more business is done on a global scale. Those managing a globally competitive business requires flexibility, quality and low-cost production. Thus managers want production processes that help them to organise as efficiently as possible from a technical perspective.

In terms of different models of management, at a basic level we can think of management as the way in which enterprises add value to inputs. Building on this, several perspectives can be taken with no single model offering a complete solution. Models reflect their context in terms of the most pressing issues facing managers at the time. To give one example, sometimes manufacturing efficiency is necessary but not sufficient. Drucker (1954) observed that customers do not buy products, but the satisfaction of needs: what they value may be different from what producers think they are selling. Managers, Drucker argued, should develop a marketing mindset, focused on what customers want, and how much they will pay. As a consequence of business becoming more global (again partly as a consequence of the Web) managers need to react quickly to international trends of changing customer needs and how to scale up to take advantage of global opportunities.

Boddy also discusses the concept of the corporate organization from a management perspective. Just as the Web is compared to the neural functions of brains, organisms, culture, machine, so is a business.

I was also struck by the interdependent links drawn between management and technology (as mentioned above) as compared with our discussions with Cathy in relation to science and technology. For example, operational research teams set up to pool the expertise of scientific disciplines are now used to help run complex civil organisations.

But, like with the Web, technology is only part of the solution. A key plank of management is human relations. Management solutions lie in reconciling technology and social needs (i.e. appreciating that work systems are socio-technical in nature). So whereas I had previously been concentrating on the Web in its influence on external business strategies, this can only be appreciated by considering how it has also revolutionized internal operations, in addition to the links between the two and the outside world which provides inputs (what Boddy calls the ‘open models’ system conception of an organisation).

In a nutshell, I have learnt that management is about relationships between subsystems and whole systems. To what extent, I wonder, is the Web breaking down the boundaries between these and blurring the conceptualization of an internal world / external world hard-line divide in business (i.e. now that consumers can become producers of certain products/services and more flexible and freelance working practices are becoming the norm)?

Basic concepts: Economics no comments

“A social science what studies the choices individuals, businesses, governments and entire societies make as they cope with scarcity and the incentives that influence.” Scarcity refers to not having enough money for food, or the inability to do something that you want to do because you have to work. We all face scarcity, but we need to make choices to cope with it, for example, choosing to work over choosing a fun activity because you need the money from working to pay bills. The choices we make are influenced by incentives. It can take the form of a reward or a penalty. If skipping work has a good opportunity of getting a much better job we may be more likely to choose to skip work. This is a just a very simple example, but it also works on a larger scale. If the price of computers drops we may as a society decide to buy more and furnish all schools with good computers.

Economics is a large area is we take into consideration individuals, businesses and entire societies; therefore it is broken up into Microeconomics (individuals and business choices) and Macroeconomics (national and global economy).

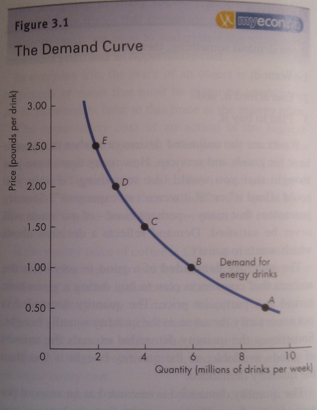

One of the most common economic phrases is “supply and demand”. Demand refers to the relationship between how many people want a product and how much it costs. Supply refers to the relationship between the quantity of the product created and its price. An increase in demand would mean an increase in price and quantity supplied. An increase in supply would mean a decrease in price and increase in quantity required.

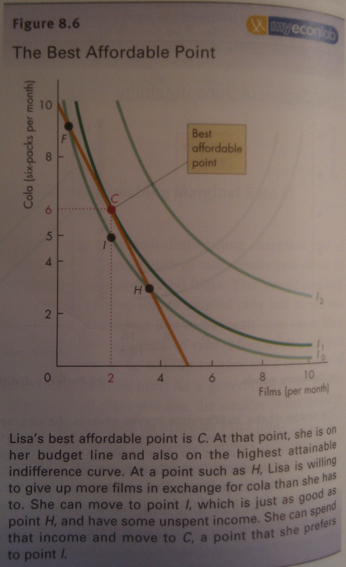

Household consumption choices are limited by income. The budget line is a way of seeing income that can be spent and how it can be spent. If prices of items you buy drop or income increases the Budget Line will change.

Indifference curves are used to show within what combinations of goods the consumer is indifferent to having. For example someone may not mind swapping a packet of cigarettes for an extra drink at the bar or even extra chocolate during the week at work.

Marginal Rate of Substitution is the rate someone will give up n of x to get n of y. If the rate is high an individual will give up a large quantity of x for a small quantity of y. This works the other way round if the rate is low, they will only give up a small quantity of x for a large quantity of y. However, we must be aware that the substitution must compliment or be a fair substitute for the item. If you are very thirsty and are offered a truck load of peanuts for one can of drink you may still decide to keep the drink!

By using these three ideas we can develop a model to predict consumer behaviour. We assume someone will pick the point that benefits them the most, so if it fits inside the budget line (indicating it is affordable) and it lies on the indifference curve (indicating it is a option someone would be happy with) and has a marginal rate of substitution that is equal to the relative price of the items desired, this gives the most affordable point and hopefully that is what someone would choose.

Elasticity is the measurement of how variables can affect each other. An example would be lowering prices to sell more.

Market power refers to the ability to influence the market. A monopoly is when a company has goods or services with no close substitute and has a barrier stopping other companies selling similar products or services. An example would be energy suppliers or the Post Office. Barriers stopping other companies could be a government contract or patent or copyright issues.

Advertising increases total cost of a product, but if the advertising increases sales the total cost of a product will fall.

Uncertainty and Risk

Uncertainty is linked to how certain you are of an event occurring. For example a farmer can never be certain crops planted will grow because they cannot be certain of the weather and other factors that could affect crop growth. Risk is a situation where more than one outcome may occur and the probability of those happening. Probability can be measured accurately or we may have to look at past experience and make a judgement called subjective probability. The cost of risk can be accessed from these probabilities. A person’s attitude towards risk can be assessed using their wealth and how much utility someone attaches to a given amount of wealth. The more wealth you have the higher the utility and the larger risks can be made.

Microeconomics

If the aim of a company is to maximise profit. They can be in any of the below modes of operation:

- Make an economic profit (average total cost is less than the price of each product)

- Make a normal profit (where economic profit is zero)

- If the price is between average total cost and average variable cost the company is loss-minimising. By continuing to produce it may still recover, if it stops it will lose money.

- If the price is below the average variable cost the company should go into shutdown. Losses are minimised by not producing more (wasting money of products that are selling at a loss).

Information and graphs summarised from:

Parkin, M., Powell, M., & Matthews, K. (2008). Economics. Essex, England: Pearson Education Limited.

.

From a Psychology background I can’t help but stick this in to reflect upon. In order to utilise economics you are assuming that the consumer or the company has the aim of maximising profits and that they will always make the best rational decision. However, luck and cognitive dissonance may be more of a factor than simply “working out the numbers”. Daniel Kahneman: How cognitive illusions blind us to reason.